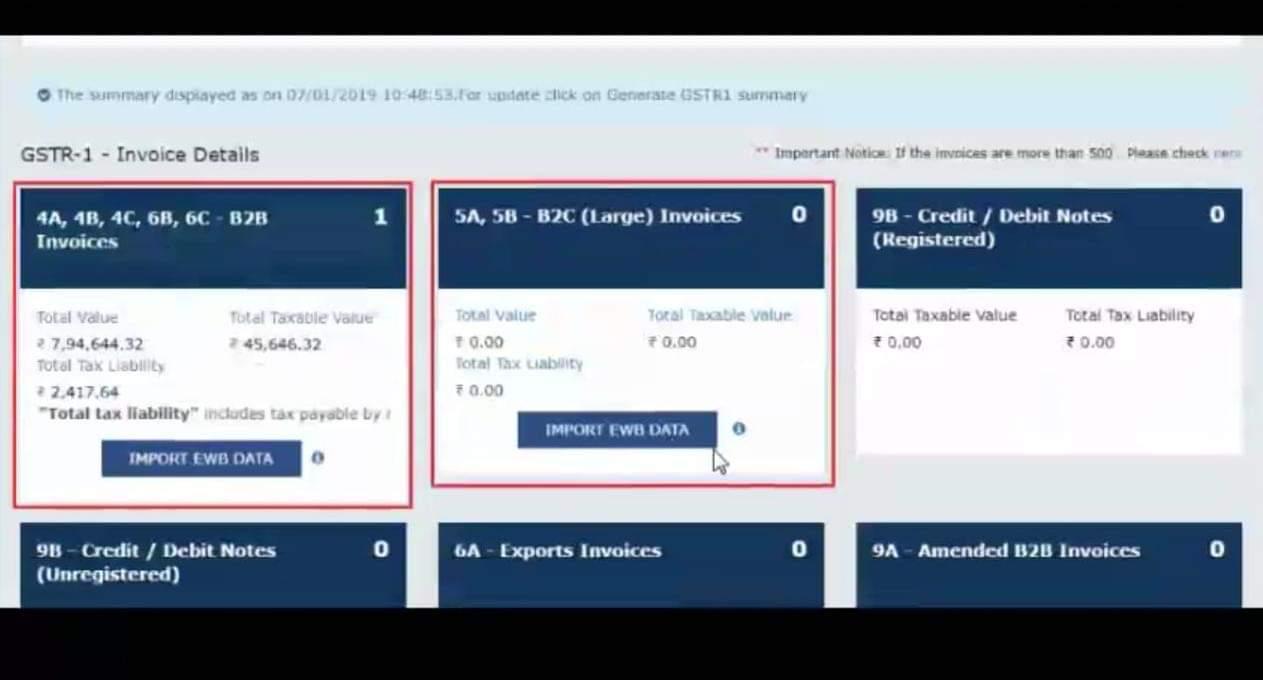

EWayBill Now you can directly import invoices declared in E-Way Bill system into form GSTR-1

EWayBill Now you can directly import invoices declared in E-Way Bill system into form GSTR-1

👇👇👇👇👇

GST Tax Consultant In Bhopal

GST Tax Consultant In Bhopal

EWayBill Now you can directly import invoices declared in E-Way Bill system into form GSTR-1

👇👇👇👇👇

Cabinet approves creation of the National Bench of the Goods and Services Tax Appellate Tribunal (GSTAT)

Posted On: 23 JAN 2019 3:48PM by PIB Delhi

The Union Cabinet, chaired by the Prime Minister Shri Narendra Modi, has approved the creation of National Bench of the Goods and Services Tax Appellate Tribunal (GSTAT).

The National Bench of the Appellate Tribunal shall be situated at New Delhi. GSTAT shall be presided over by its President and shall consist of one Technical Member (Centre) and one Technical Member (State).

The creation of the National Bench of the GSTAT would amount to one time expenditure of Rs.92.50 lakh while the recurring expenditure would be Rs.6.86 crore per annum.

Details:

Goods and Services Tax Appellate Tribunal is the forum of second appeal in GST laws and the first common forum of dispute resolution between Centre and States. The appeals against the orders in first appeals issued by the Appellate Authorities under the Central and State GST Acts lie before the GST Appellate Tribunal, which is common under the Central as well as State GST Acts. Being a common forum, GST Appellate Tribunal will ensure that there is uniformity in redressal of disputes arising under GST, and therefore, in implementation of GST across the country.

Chapter XVIII of the CGST Act provides for the Appeal and Review Mechanism for dispute resolution under the GST Regime. Section 109 of this Chapter under CGST Act empowers the Central Government to constitute, on the recommendation of Council, by notification, with effect from such date as may be specified therein, an Appellate Tribunal known as the Goods and Services Tax Appellate Tribunal for hearing appeals against the orders passed by the Appellate Authority or the Revisional Authority.

Outcome of 32nd GST Council Meeting -FM Arun Jaitley press meet

*1. Threshold limit increased to 40 Lakhs*

Effective April 1, the GST exemption threshold has been raised from Rs 20 lakh to Rs 40 lakh. For hilly states and those in the North East, the threshold has been doubled to Rs 20 lakh.

*Earlier in a press talk AP FM said increased to 50lakhs, but it is increased to 40lakhs only as said by FM*

*2. Power to states*

Now states will be able to choose if they want to keep the GST exemption limit at Rs 20 lakh or Rs 40 lakh, Jaitley said.

*3. Composition limit increased to 1.5Cr from the present 1 cr*

The existing Composition Scheme turnover threshold raised to Rs 1.5 crore.

Those who use the scheme from April 1,2019

*4 Quarterly payment and Annual Return*

Now Composition tax payers will pay tax quarterly, but file returns annually.

*5 Composition scheme for services*

Those providing services or mixed supplies (goods and services) with a turnover up to Rs 50 lakhs will now be entitled to avail composition scheme.

*6 Rate for services under comp scheme @ 6%*

Compounding rate for services under composition scheme is fixed at 6 percent.

*7 RealEstate*

A committee has been set up to consider real estate GST rates, a consensus is yet to be achieved, says FM Arun Jaitley.

*8 Calamity cess by Kerela @1%*

GST Council lets Kerala levy 1% cess for 2 years on intra-state sales:

Finance Minister arun jaitley.

32बी जीएसटी कॉउंसलिंग मीटिंग में लिए जा सकते है ये महत्वपूर्ण निर्णय

*2019 का जीएसटी तोहफ़ा*

*GST Gift 2019*

🔥 केरल को गुड्स एंड सर्विसेज़ पर दो साल के लिए 1% कैलमिटी सेस (डिज़ास्टर टैक्स) लगाने की छूट सम्भव

Kerala may charge 1% calamity cess for two years on Goods and Services.

🔥 कंपोजिशन डीलर्स को त्रैमासिक टैक्स के साथ वार्षिक रिटर्न् भरने की सुविधा

Composition Dealers to make annual return filling with quarterly tax

🔥 सर्विसेज़ प्रोवाइडर्स (टर्नओवर ₹ 50 लाख) को कंपोजिशन स्कीम 5% टैक्स के साथ

Services Providers (turnover ₹ 50 lakh) composition scheme @ 5% tax

🔥 जीएसटी रजिस्ट्रेशन लिमिट को ₹ 40-50 लाख करने पर अभी सहमति नहीं

No consent on the GST registration limit to ₹ 40-50 lakh

🔥 टर्नओवर ₹ 50-60 लाख के बीच होने पर एकमुश्त ₹ 5000/- वार्षिक और

टर्नओवर ₹ 60-75 लाख के बीच होने पर एकमुश्त ₹ 10000/- से 15000/- वार्षिक

टैक्स जमा करवाने पर भी विचार

Lump sum tax ₹ 5000/ – yearly for Annual Turnover between ₹ 50-60 lakh and

Lump sum tax ₹ 10000-15000/ – yearly Annual Turnover between ₹ 60-75 lakh under Consideration

🔥 वार्षिक टर्नओवर ₹ 1.50 करोड़ वाले डीलर्स को फ्री एकाउंटिंग सॉफ्टवेयर देने का भी विचार

Ideas for giving free accounting software to dealers turnover upto ₹ 1.50 crore annually

*Disclaimer*

Wait for 32nd GSTC Meet

GST (Amendment) Act, 2018

The President has given its assent to the The Central Goods and Services Tax (Amendment) Act 2018 , The Integrated Goods and Services Tax (Amendment) Act 2018. , The Union Territory Goods and Services Tax (Amendment) Act 2018. , The Goods and Services Tax (Compensation to States) Amendment Act 2018. on August 29, 2018.

Effective Date for Amendment in GST Act(s) 2018 will be 01.02.2019

Changes in CGST Act 2017 w.e.f 01.02.2019

Following are the Changes in the Relevant Section of CGST Act 2017 by Central Goods and Services Tax (Amendment) Act 2018

Section 2(4). Definitions of CGST Act 2017 : Adjudicating Authority

Section 2(17). Definitions of CGST Act 2017 : business

Section 2(18). Definitions of CGST Act 2017 :business vertical

Section 2(35). Definitions of CGST Act 2017 : cost accountant

Section 2(69). Definitions of CGST Act 2017 : local authority

Section 2(102). Definitions of CGST Act 2017 : services

Section 7. Scope of supply. : Amended relating to “Scope of Supply” in order to clarify the scope of supply.

Section 9. Levy and collection. : Amended so as to restrict the levy of tax on reverse charge basis to receipt of supplies of certain specified categories of goods or services or both by notified classes of registered persons from unregistered suppliers on the recommendations of the Council.

Section 10. Composition levy. : Amended so as to raise the statutory threshold of turnover for a taxpayer to be eligible for the composition scheme from one crore rupees to one crore and fifty lakh rupees, and to allow the composition taxpayers to supply services (other than restaurant services), for up to a value not exceeding ten per cent. of turnover in the preceding financial year, or five lakh rupees, whichever is higher.

Section 12. Time of supply of goods. : Amended and the said amendment is drafting in nature.

Section 13. Time of supply of services. : Amended and the said amendment is drafting in nature.

Section 16. Eligibility and conditions for taking input tax credit. :

Amended in order to provide for input tax credit in cases of “Bill- to-ship-to” model in the case of supply of services. The said Amendment further seeks to include the provisions relating to the new return format as specified in the proposed new section 43A, for availment of input tax credit.

Section 17. Apportionment of credit and blocked credits. : :Amended in order to further expand the scope of eligibility of input tax credit.

Section 20. Manner of distribution of credit by Input Service Distributor. : Amended in order to exclude the amount of tax levied under Entry 92A of List I of the Seventh Schedule of the Constitution from the value of turnover for the purposes of distribution of credit.

Section 22. Persons liable for registration. : Amended so as to increase the threshold turnover for registration in special category States of Arunachal Pradesh, Assam, Himachal Pradesh, Meghalaya, Sikkim and Uttarakhand from ten lakh rupees to twenty lakh rupees.

Section 24. Compulsory registration in certain cases. : Amended so as to provide for mandatory registration for only those e-commerce operators who are liable to collect tax at source under section 52 of the Act.

Section 25. Procedure for registration. : Amended aso as to allow persons having multiple places of business in a State or Union territory to obtain separate registration for each such place of business, and to insert the provisions for separate registration for a person having a unit(s) in a Special Economic

Zone or being a Special Economic Zone developer, distinct from his other units located outside the Special Economic Zone.

Section 29. Cancellation of registration. Amended so as to provide for temporary suspension of registration while cancellation of registration is under process.

Section 34. Credit and debit notes. Amended so as to allow registered persons to issue consolidated credit or debit notes in respect of multiple invoices issued in a Financial Year.

Section 35. Accounts and other records. Amended so as to provide that any Department of the Central or State Government or local authority which is subject to audit by the Comptroller and Auditor-General of India need not get their books of account audited by any Chartered Accountant or Cost Accountant.

Section 39. Furnishing of returns. : Amended so as to provide for prescribing the procedure for quarterly filing of returns with monthly payment of taxes.

Section 43A: Procedure for furnishing return and availing input tax credit. (Newly inserted)

Section 48. Goods and services tax practitioners : Amended so as to allow Goods and Services Tax Practitioners to perform other functions such as filing refund claim, filing application for cancellation of registration, etc.

Section 49. Payment of tax, interest, penalty and other amounts. Amended in order to provide that the credit of State tax or Union territory tax can be utilised for payment of integrated tax only when the balance of the input tax credit on account of central tax is not available for payment of integrated tax.

Section 49A : Utilisation of input tax credit subject to certain conditions (Newly inserted) This Section seeks to specify that a taxpayer would be able to utilise the input tax credit on account of central tax, State tax or Union territory tax only after exhausting all the credit on account of integrated tax available to him towards payment or integrated tax, Central tax, State tax or Union territory tax.

Section 49B :Order of utilisation of input tax credit. (Newly inserted) This Section seeks to empower the Government to prescribe any specific order of utilisation of input tax credit of any of the taxes for payment of any tax.

Section 52. Collection of tax at source. : Amended in order to give the reference of section 39 of CGST Act 2017 Furnishing of Returns

Section 54. Refund of tax. Amended in order to provide that the principle of unjust enrichment will apply in case of a refund claim arising out of supplies of goods or services or both made to a Special Economic Zone developer or unit, and to allow receipt of payment in Indian rupees, where permitted, by the Reserve Bank of India in case of export of services.

Section 79. Recovery of tax. Amended to enable recovery to be made from distinct persons registered in different States or Union territories in order to ensure speedy recovery from other establishments of the registered person.

Section 107. Appeals to Appellate Authority. Amended Authority”, in order to specify twenty-five crore rupees as the upper limit of the amount of pre-deposit payable for filing of appeal before the Appellate Authority.

Section 112. Appeals to Appellate Tribunal. Amended in order to specify fifty crore rupees as the upper limit of the amount of pre-deposit payable for filing of appeal before the Appellate Tribunal.

Section 129. Detention, seizure and release of goods and conveyances in transit Amended in order to increase the time limit before which proceedings under section 130 can be initiated from seven to fourteen days.

Section 140. Transitional arrangements for input tax credit. Amended in order to clarify with retrospective effect from 1st July, 2017 that the cesses and additional duty of excise (on textile and textile articles) levied under the pre-Goods and Services Tax laws shall not be a part of transitional input tax

credit under the goods and services tax.

Section 143. Job work procedure. Amended in order to empower the Commissioner to extend the time limit for return of inputs and capital goods sent on job work, upto a period of one year and two years, respectively.

SCHEDULE I. of CGST Act 2017 “Activities to be treated as supply even if made without consideration”. : Amended

SCHEDULE II. of CGST Act 2017 : Amended the title of Schedule II of the principal Act from “Activities to be treated as supply of goods or supply of services” to “Activities or transactions to be treated as supply of goods or supply of services”.

SCHEDULE III. of CGST Act 2017 “Activities or transactions which shall be treated neither as a supply of goods nor a supply of services”. Amended

Changes in IGST Act 2017 w.e.f 01.02.2019

Section 2(6). Definitions. “export of services

Section 2(16). Definitions. “non-taxable online recipient”

Section 5. Levy and collection. : Amended to empower the Central Government to notify classes of registered persons to pay tax on reverse charge basis in respect of receipt of supplies of certain specified Categories of goods or services or both from unregistered suppliers;

Section 8. Intra-State supply. Words ‘‘being a business vertical’’ shall be omitted.

Section 12. Place of supply of services where location of supplier and recepient is in India. : Amended to provide that if the transportation of goods is to a place outside India, the place of supply shall be the place of destination of such goods;

Section 13. Place of supply of services where location of supplier or location of receipient is outside India. Provisions of Section 13(1)(3)(a) Amended and shall not apply in the case of services supplied in respect of goods which are temporarily imported into India for repairs or for any other treatment or process and are exported after such repairs or treatment or process without being put to any use in India, other than that which is required for such repairs or treatment or process;

Section 17. Apportionment of tax and settlement of funds. Amended to make a provision for settlement of balance in the integrated tax account equally between the Central Government and the State Governments or the Union territories, as the case may be, on ad hoc basis and shall be adjusted against the amount apportioned under the said sub-sections.

Section 20. Application of provisions of Central Goods and Services Tax Act. Amended to specify the amount of pre-deposit payable

for filing of appeals —

(a) before the Appellate Authority to be capped at fifty crore rupees;

(b) before the Appellate Tribunal to be capped at one hundred crore rupees.